Developments in the steel market

Outlook steel market

The Global Economy is expected to remain stable. World GDP will grow by +3.2%* in 2025. The outlook continues to differ across countries, with weaker outcomes in advanced economies, especially in Europe, and growth in the US and emerging economies. Therefore, global steel demand will fall in 2024 and increase slightly in 2025.

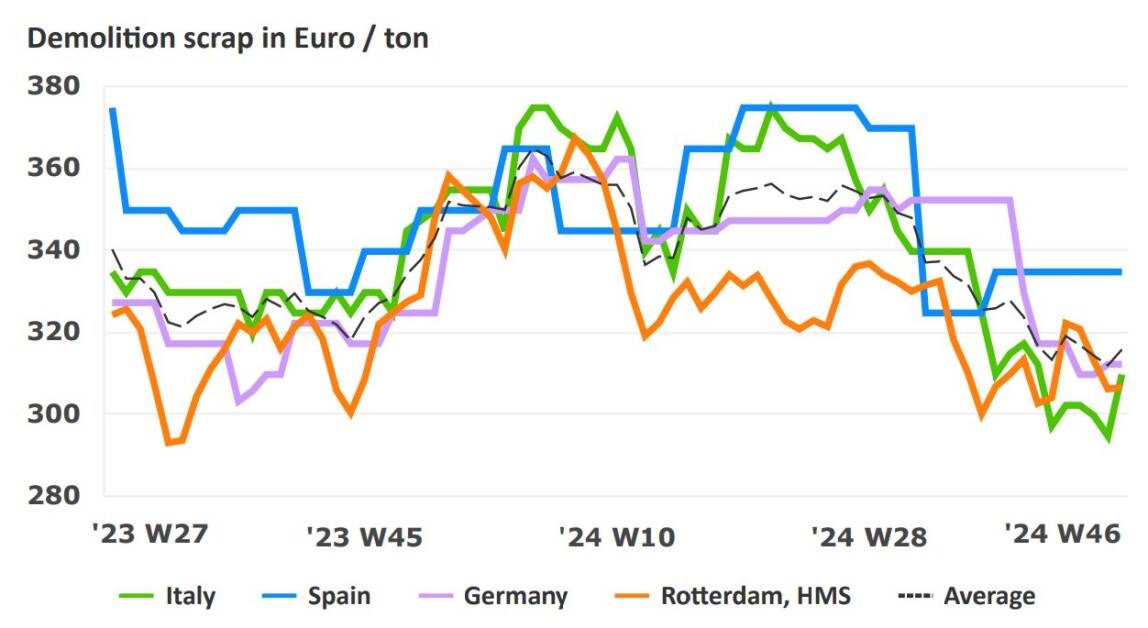

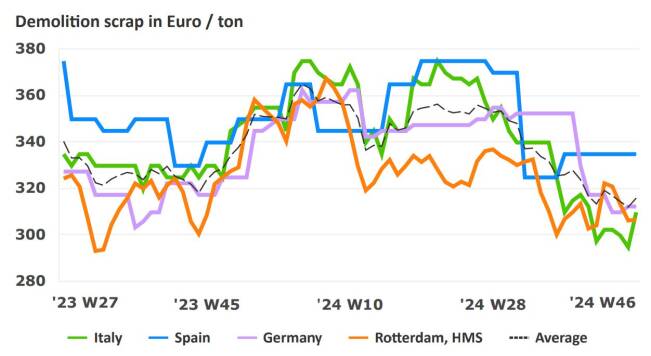

In Europe, the market situation is still challenging with further demand decline in the second half year 2024. Several companies went for extended summer closure to adjusted capacities. The manufacturing industry is influenced by geopolitical uncertainties and declining household purchasing power. Construction industry was influenced by monetary activities to control the inflation rate. In addition, destocking has continued at high level, reflecting poor steel demand. The biggest European economy Germany is struggling to pull the economy out of recession. The automotive market has decreased, Volkswagen and further automotive suppliers have announced restructuring measures.

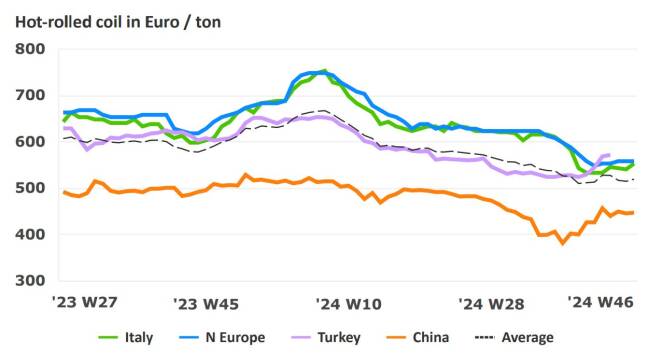

In line with the market situation described above, it is not surprising that the price levels for pipes & tubes are hardly changing. Raw material prices remained almost stable. Scrap prices showed no significant changes. Price levels for European hot-rolled coils increased slightly. Import offers are not seen as interesting to EU users due to lead times, safeguard quota and potential anti-dumping risk. The delivery times for most product groups have not changed and are in line with the market.

In Europe, the market situation is still challenging with further demand decline in the second half year 2024. Several companies went for extended summer closure to adjusted capacities. The manufacturing industry is influenced by geopolitical uncertainties and declining household purchasing power. Construction industry was influenced by monetary activities to control the inflation rate. In addition, destocking has continued at high level, reflecting poor steel demand. The biggest European economy Germany is struggling to pull the economy out of recession. The automotive market has decreased, Volkswagen and further automotive suppliers have announced restructuring measures.

In line with the market situation described above, it is not surprising that the price levels for pipes & tubes are hardly changing. Raw material prices remained almost stable. Scrap prices showed no significant changes. Price levels for European hot-rolled coils increased slightly. Import offers are not seen as interesting to EU users due to lead times, safeguard quota and potential anti-dumping risk. The delivery times for most product groups have not changed and are in line with the market.

*Source: International Monetary Fund from November 2024

Carbon Border Adjustment Mechanism (CBAM) and the impact on the market for steel tube products.

CBAM stands for Carbon Border Adjustment Mechanism. It is an EU regulation for the correction of CO2 emissions at its border, released during the production of six product categories: iron and steel, cement, fertilizers, aluminum, electricity and hydrogen. The CBAM also applies to our assortment of steel pipes, fittings, flanges and bar steel.

Please read further details on our website:

www.vanleeuwen.com/en/carbon-border-adjustment-mechanism-cbam-and-the-impact-on-the-market-for-steel-tube-products/

CBAM stands for Carbon Border Adjustment Mechanism. It is an EU regulation for the correction of CO2 emissions at its border, released during the production of six product categories: iron and steel, cement, fertilizers, aluminum, electricity and hydrogen. The CBAM also applies to our assortment of steel pipes, fittings, flanges and bar steel.

Please read further details on our website:

www.vanleeuwen.com/en/carbon-border-adjustment-mechanism-cbam-and-the-impact-on-the-market-for-steel-tube-products/

Update anti-dumping investigation on imports of seamless pipes and tube

The European Commission has launched a new anti-dumping investigation* on imports of seamless pipes and tube from China. The investigation has been initiated following the complaint of the European Steel Tube Association (ESTA) on April 2nd, 2024. The complaint alleges that imports of certain seamless pipes & tubes are being dumped and thereby causing injury to the Union industry. The investigation period could take up to 14 months, with the possibility of provisional duties.

For seamless pipes & tubes, the price levels remain stable pending the completion of the investigation. Several mills have reduced production capacity or implemented shorter working hours in response to low demand.

**Source: Official Journal of the European Union C/2024/3225 from 17.5.2024

The European Commission has launched a new anti-dumping investigation* on imports of seamless pipes and tube from China. The investigation has been initiated following the complaint of the European Steel Tube Association (ESTA) on April 2nd, 2024. The complaint alleges that imports of certain seamless pipes & tubes are being dumped and thereby causing injury to the Union industry. The investigation period could take up to 14 months, with the possibility of provisional duties.

For seamless pipes & tubes, the price levels remain stable pending the completion of the investigation. Several mills have reduced production capacity or implemented shorter working hours in response to low demand.

**Source: Official Journal of the European Union C/2024/3225 from 17.5.2024

Update anti-dumping investigation on imports of seamless pipes and tube

The European Commission has launched a new anti-dumping investigation* on imports of seamless pipes and tube from China. The investigation has been initiated following the compliant of the European Steel Tube Association (ESTA) on April 2nd, 2024. Content of the compliant is that imports of certain seamless pipes & tubes are being dumped and thereby causing injury to the Union industry. The investigation period could take up to 14 months, with the possibility of provisional duties.

For seamless pipes & tubes, the price level is stable, because the investigation has not been completed. Several mills have reduced production capacity or introduced shorter working hours due to low demand.

**Source: Official Journal of the European Union C/2024/3225 from 17.5.2024

The European Commission has launched a new anti-dumping investigation* on imports of seamless pipes and tube from China. The investigation has been initiated following the compliant of the European Steel Tube Association (ESTA) on April 2nd, 2024. Content of the compliant is that imports of certain seamless pipes & tubes are being dumped and thereby causing injury to the Union industry. The investigation period could take up to 14 months, with the possibility of provisional duties.

For seamless pipes & tubes, the price level is stable, because the investigation has not been completed. Several mills have reduced production capacity or introduced shorter working hours due to low demand.

**Source: Official Journal of the European Union C/2024/3225 from 17.5.2024

Carbon Border Adjustment Mechanism (CBAM) and the impact on the market for steel tube products.

CBAM means Carbon Border Adjustment Mechanism. It is an EU regulation for the correction of CO2 emissions at its border, released during the production of six product categories: iron and steel, cement, fertilizers, aluminum, electricity and hydrogen. The CBAM also applies to our assortment of steel pipes, fittings, flanges and bar steel.

Please read further details on our website:

www.vanleeuwen.com/en/carbon-border-adjustment-mechanism-cbam-and-the-impact-on-the-market-for-steel-tube-products/

CBAM means Carbon Border Adjustment Mechanism. It is an EU regulation for the correction of CO2 emissions at its border, released during the production of six product categories: iron and steel, cement, fertilizers, aluminum, electricity and hydrogen. The CBAM also applies to our assortment of steel pipes, fittings, flanges and bar steel.

Please read further details on our website:

www.vanleeuwen.com/en/carbon-border-adjustment-mechanism-cbam-and-the-impact-on-the-market-for-steel-tube-products/

*Source: International Monetary Fund from November 2024

The Global Economy is expected to remain stable. World GDP will grow by +3.2%* in 2025. The outlook continues to differ across countries, with weaker outcomes in advanced economies, especially in Europe, and growth in the US and emerging economies. Therefore, global steel demand will fall in 2024 and increase slightly in 2025.

In Europe, the market situation is still challenging with further demand decline in the second half year 2024. Several companies went for extended summer closure to adjusted capacities. The manufacturing industry is influenced by geopolitical uncertainties and declining household purchasing power. Construction industry was influenced by monetary activities to control the inflation rate. In addition, destocking has continued at high level, reflecting poor steel demand. The biggest European economy Germany is struggling to pull the economy out of recession. The automotive market has decreased, Volkswagen and further automotive suppliers have announced restructuring measures.

In line with the market situation described above, it is not surprising that the price levels for pipes & tubes are hardly changing. Raw material prices remained almost stable. Scrap prices showed no significant changes. Price levels for European hot-rolled coils increased slightly. Import offers are not seen as interesting to EU users due to lead times, safeguard quota and potential anti-dumping risk. The delivery times for most product groups have not changed and are in line with the market.

In Europe, the market situation is still challenging with further demand decline in the second half year 2024. Several companies went for extended summer closure to adjusted capacities. The manufacturing industry is influenced by geopolitical uncertainties and declining household purchasing power. Construction industry was influenced by monetary activities to control the inflation rate. In addition, destocking has continued at high level, reflecting poor steel demand. The biggest European economy Germany is struggling to pull the economy out of recession. The automotive market has decreased, Volkswagen and further automotive suppliers have announced restructuring measures.

In line with the market situation described above, it is not surprising that the price levels for pipes & tubes are hardly changing. Raw material prices remained almost stable. Scrap prices showed no significant changes. Price levels for European hot-rolled coils increased slightly. Import offers are not seen as interesting to EU users due to lead times, safeguard quota and potential anti-dumping risk. The delivery times for most product groups have not changed and are in line with the market.

Outlook steel market

Developments in the steel market